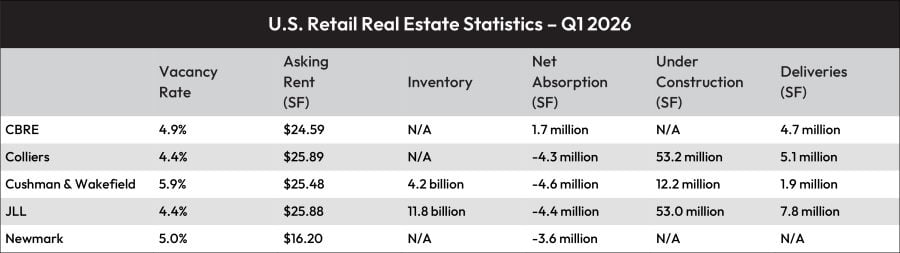

The Q1 2026 retail reports agreed on several things. First, negative net absorption rates were reported across all five write-ups, with the lone exception being CBRE’s “U.S. Retail Figures.” Still, “multiple bankruptcy filings triggered a wave of closures, which added available space to the market,” the CBRE analysts explained.

Second, those bankruptcy backfills are being snapped up by what Colliers “U.S. Retail Figures” write-up called steady demand, adding that a “clear bifurcation persists, with tight availability for spall spaces and more modest availability among large anchor boxes.

Third, the construction pipeline continues to dwindle. JLL, in its “Retail Market Dynamics” report, said that gross deliveries of 7.8 million square feet were “partially offset by 2.6 million square feet of demolitions, comprising obsolete department stores and underperforming strip centers. As a result, net new supply “equated to roughly 5.2 million square feet for the quarter,” the JLL analysts said.

Additional reasons were given for flat rent growth and negative absorption. Newmark’s “Retail Market Conditions & Trends” said that market uncertainty didn’t help matters as “consumer sentiment continues to be negatively affected by lingering inflation, uncertainty about the job market and the impact of the Iran conflict on fuel costs and potentially other prices.” Still, Newmark analysts and others said that retail sales and consumer spending remain in positive territory.

Meanwhile, Cushman & Wakefield’s “MarketBeat” said that first quarters are generally slower for retail leasing, while “severe winter weather may have curtailed activity more than normal this year.”

As for the outlook, all the reports said that continued supply shortages will continue to exert pressure on rent growth. At the same time, consumer sentiment is worth keeping an eye on. “If elevated oil prices persist, higher costs for gasoline, utilities and consumer products are likely to weigh on household budgets and consumer confidence in Q2 and potentially longer,” said Cushman & Wakefield analysts.

JLL added that the supply situation isn’t likely to change anytime soon, adding that “location will matter more than the national average.” All the reports said that the Sun Belt markets outpaced the rest of the country in retail metrics, driven by population growth. “For the remainder of 2026, performance will be less about the market overall, and more about which markets a portfolio is in,” JLL researchers added.

Colliers forecast that limited supply, combined with robust demand, means a quick backfill, though Newmark analysts noted that backfill activity isn’t showing signs of slowing.

Newmark added that stagnant, older retail space could make the case for additional retail construction. But with construction costs still high and rents unable to justify new development, opportunities could exist in redeveloping underperforming centers “through redesign or mixed-use conversion,” which will remove outdated space from the market and “ultimately reduce the total retail footprint,” Newmark researchers said.

Meanwhile, as retailers are likely to remain cautious about near-term leasing while they monitor consumer conditions, Cushman & Wakefield researchers indicated that a broad pullback is unlikely.

“Assuming easing energy prices and a resilient labor market with only modest unemployment increases, retail demand should remain resilient, supporting vacancy stabilization through year-end,” they added.

The post Retail Q1: Low Availability and Construction Slow Absorption appeared first on Connect CRE.