When Babylist’s founder and CEO, Natalie Gordon, was growing up, she wasn’t always excited about opening her Christmas and birthday presents. Every year, members of her family—especially her grandmother—would contribute money to her college fund. Today, she’s grateful they did.

“On a personal level, it was really meaningful. The experience shaped how I view long-term gifting,” Gordon says.

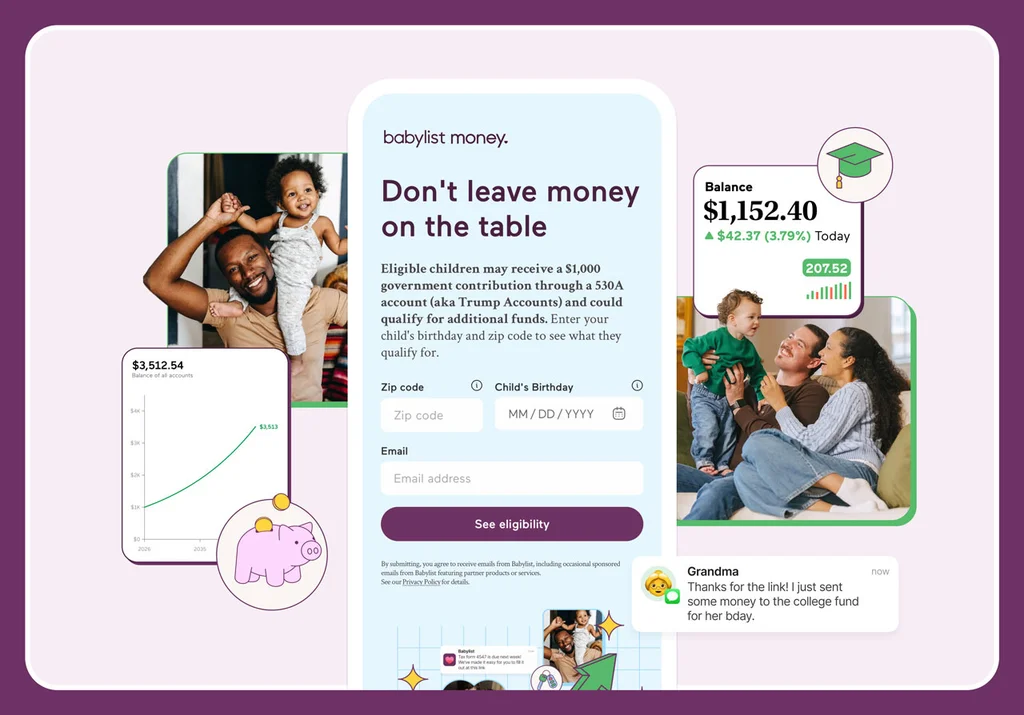

Now, her baby registry company—which has built a $750-million-a-year business helping parents create and distribute registries, order items from retailers, and receive them when they want—is trying to get customers to adopt her family’s behavior at scale. The first step? Helping parents and sponsors set up so-called Trump accounts.

The new accounts are more formally known as 530A accounts after the relevant section of the Internal Revenue Code. They let parents and sponsors of children born in the U.S. create an investment vehicle for them that will not be taxed annually. Children born between January 1, 2025, and December 2028 can also receive a $1,000 contribution from the Treasury Department to give them a head start. Families and employers can contribute a maximum of $5,000 annually to the fund, which the child can access only when they turn 18.

The app for these accounts launched yesterday, built by Bank of New York Mellon and Robinhood. (In the future, parents will be able to roll them over to other financial institutions.) Parents can enroll at Trumpaccounts.gov, and will be able to begin funding them in July.

For many parents, the process of setting up one of these accounts and contributing to it can be daunting. That’s why Babylist launched a money hub in mid-2026 with all the information parents need.

“The information around these accounts has rolled out very slowly. It’s been confusing not only for eligible families but for the entire financial services industry. Even industry leaders didn’t have clear answers,” Gordon says.

An information and gifting hub

The company’s Babylist Money content hub focuses on what new parents need to know. “We’ve answered questions like, how do you qualify? How do you access the accounts? How do they compare to existing options like 529 plans?” Gordon explains, referring to the college savings plan named for that section of the revenue code. The company has been updating information as it’s released and has built a state and zip code lookup tool for users to access the most accurate information. It also provides broader advice about saving money for children.

The tool is part of the company’s strategy to develop a relationship with families from pregnancy until a child reaches adulthood. Gordon is betting that customers who have trusted the service to help them during one of the most important times in their lives—their child’s birth—are likely to trust them again as they prepare for the next 18 years.

Gordon says one of the inspirations for the money hub was a “wish list” service that the company launched a few years ago. It allows families—and even children—to create lists of gift ideas for holidays and birthdays. “We think the future of wish lists and education savings could converge,” Gordon says. “More broadly, we want to go beyond just milestone events. Parents continue needing support after the registry ends, and we help them navigate that next phase.”

Babylist Money offers advice and educational social media content that outlines how to sign up for these accounts and what the funds can be invested in. The company also recently launched a family finance-focused podcast, Family Money, which will feature discussions about the cost of raising kids along with saving strategies for families.

The platform will also help parents solicit contributions to their child’s Trump accounts around milestones, much as Gordon’s family helped fund her savings account. Babylist will help parents send email blasts or share the option via text with friends and family—and remove the awkwardness around asking for such support.

“We believe financial support shouldn’t fall only on parents—it should include friends and family. But right now, asking for money for college can feel awkward and not very joyful compared to buying a gift,” Gordon says.

“We understand gifting extremely well,” she says. “The challenge is making college contributions feel as natural and delightful as giving a physical gift. We want to make that experience easy for both the giver and the parent.”

Financial literacy and services

Babylist, which grew revenue 45% in 2025, has been expanding beyond its core baby registry business in recent years. In 2022, it launched Babylist Health to help parents get insurance-covered breastpumps. Babylist also opened an experiential retail store in Los Angeles; another location will open in New York later this year.

Babylist won’t make money from helping families set up Trump accounts. Instead, it’s using the platform to attract new parents and convert them into customers. The hub also keeps existing customers engaged.

Already, Babylist emails about the 530A accounts have seen click-through rates that are two to three times as high as a typical email campaign from the company. When a 30-second ad about the accounts aired ahead of this year’s Super Bowl (paid for by a nonprofit advocacy group), Babylist launched a push notification campaign from its app. It generated more than 20,000 downloads of the company’s No Fuss Guide to Trump Accounts.

Educational content about the accounts on the site has also driven more than 650,000 visits in the past three months.

With more than 3.6 million children born in the U.S. in 2025 alone, Babylist sees a big opportunity to keep consumers coming to its platform. More than 10 million people made purchases through Babylist in 2025, and the company says that 22% of expecting families in the U.S. use the platform.

Gordon says that the Trump accounts hub is just the beginning for the company’s push into financial literacy and services. “Right now, we’re focused on education savings because this moment is changing behavior,” she says. “But families face many financial decisions—insurance, wills, trusts, major purchases like homes or cars—and we want to play a role in those areas over time.”