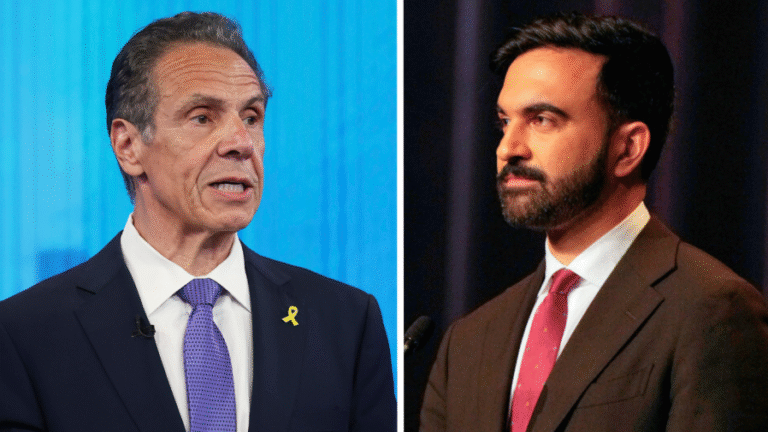

The possibility that President Trump could replace Federal Reserve Chair Jerome Powell with Treasury Secretary Scott Bessent is spinning heads from Washington to Wall Street and beyond.

Senators on both sides of the aisle have thrown cold water on the idea despite rising tension between Trump and Powell over interest rates, and the precedent-breaking move could also rock markets and face legal challenges.

Here’s a look at the political and financial feasibility of Bessent doubling down with two of the most important government roles in finance.

First of all, is it legally possible?

Legal experts say there’s no law preventing the Treasury secretary from also serving as the chair of the Federal Reserve.

“There’s no prohibition in the Federal Reserve Act that says a member of the board of governors, or the chair, can’t also be the Secretary of the Treasury,” Sarah Binder, a senior fellow at the Brookings Institution, told The Hill.

Treasury secretaries used to sit on the board of the Fed prior to 1935.

However, having a dual Fed-Treasury chief would fly in the face of the doctrine of central bank independence that has gotten stronger over the years.

Specifically, it would undermine a semi-formal 1951 agreement between the two entities that separated the duties of public debt issuance from interest-rate setting.

The nearly 75-year accord made it so that the Treasury Department would manage bonds and the debt, and the Fed would handle interest rates and the money supply. This was to protect against the temptation of printing money to pay for the debt.

“The announcement [of the agreement referred] to a ‘full accord with respect to debt-management and monetary policies,’” Columbia Law professor Lev Menand and New York Fed policy adviser Joshua Younger wrote in the Columbia Law Review in 2023.

The separation of these duties is still passionately supported by many.

“You don’t want the fiscal authority making decisions about interest rates,” Binder told The Hill.

Would markets tolerate it?

Bond markets got woozy in response to Trump’s trade policies earlier this year and the administration course corrected as a result.

National Economic Council chief Kevin Hassett said the White House moved up its pause of wide-ranging “reciprocal” tariffs after the bond market cratered.

“There’s no doubt that the Treasury market yesterday made it so that the decision – it was about time to move – was made with perhaps a little more urgency,” he said after the pause.

Stock markets also buckled and bounced this week following a new extension of the “reciprocal” import tax deadline to Aug. 1.

Some policy analysts don’t believe the markets would tolerate a dual Fed-Treasury head because it would subvert the central bank’s independence.

“I don’t think the market would react [well] to that. Even if it was someone they respected, it just too overtly undermines the independence of the Fed,” Stephen Myrow, a managing partner at Beacon Policy Advisers, told The Hill. “I don’t think they would do that.”

The real worry is inflation

Fed independence encapsulates the idea that part of the central bank’s job is to crush inflation even though actions to do so can increase unemployment, start recessions and sometimes be politically unpopular.

Inflation is often seen as a greater evil than unemployment because it can be politically and socially destabilizing.

By undermining Fed independence with a dual Fed-Treasury chair, the worry is that Bessent will bend to Trump’s calls to cut interest rates and that the Fed will be more tolerant of inflation, similar to the dynamic between former president Richard Nixon and his Fed chair, Arthur Burns.

Inflation tolerance is of particular concern following the post-pandemic inflation, which factored as the top issue in the 2024 election and continues to play a role in U.S. elections.

“The public is much more price sensitive now,” David Beckworth, a fellow at the Mercatus Institute, told The Hill. “People were really upset about that [inflation]. To my mind, Trump is really playing with fire here.”

Other challenges to Fed independence

The possibility of Bessent holding both roles is one of a few signs that public debts are rising over inflation as a policy priority, especially after the estimated $3.3 trillion debt bomb coming from Republicans’ tax-and-spending cut bill, which the president signed into law July 4.

Trump has recently been encouraging the Fed to lower interest rates not simply because they would make lending cheaper and juice the markets but because they would make public debt payments cheaper.

“Hundreds of billions of dollars being lost!” Trump wrote late last month on Truth Social in reference to debt service payments, again encouraging Powell to lower rates.

Sen. Ted Cruz (R-Texas) also suggested getting rid of interest payments on the $3.2 trillion in reserves that commercial banks hold now with the Fed. That could encourage them to buy bonds to get a comparable return, or the Fed could force banks to hold onto their reserves.

“That’s a form of financial repression,” Beckworth said, referring to when debts get inflated away as the rate of inflation surpasses the rate of interest.

“It’s a tax on the banks. It sounds crazy, but it’s been used in other countries,” he added.

The Fed also recently advanced a plan to change big banks’ leverage ratios. This could also encourage bond buying, which would lower long-term interest rates, just like quantitative easing.

“We want to ensure that the leverage ratio does not become regularly binding and discourage banks from participating in low-risk activities, such as Treasury market intermediation,” Powell said last month.

Warnings about ‘fiscal dominance’

The various ad hoc changes to monetary policy stemming from the debt and Trump’s attacks on the Fed — including the potential second role for Bessent — are being labeled by economists on both the right and the left as “fiscal dominance.”

In a recent op-ed published by the Washington Post, Biden administration economist Lael Brainard called the president’s debt-invoking missives to the Fed “a remarkably clear statement of what economists call fiscal dominance.”

Others don’t give that concept much credence but see the proposals as simply another attack on agency independence similar to the ones the Trump administration has carried out on other agencies like the Environmental Protection Agency, U.S. Agency for International Development (USAID), the Consumer Financial Protection Bureau and others.

“Fiscal dominance and monetary dominance are incoherent concepts,” financial researcher Nathan Tankus told The Hill. “We have one entity that has wide discretion over economic policy, and that’s the Federal Reserve.”

“It makes decisions in response to the macroeconomic environment, and that’s really the long and the short of it,” Tankus added.