A reader wrote in asking how to double his net worth, from $500,000 to $1,000,000.

Doubling a net worth of $500,000 is a significant financial milestone. Whether this happens in five years or twenty depends entirely on the levers of risk, time, and strategy. While a starting $500,000 net worth is great, these strategies work for anyone looking to grow wealth, regardless of how much money they currently have.

Here’s a comprehensive guide, which tackles the core pillars of wealth building and specific “paths” based on your personal risk profile and timeline.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

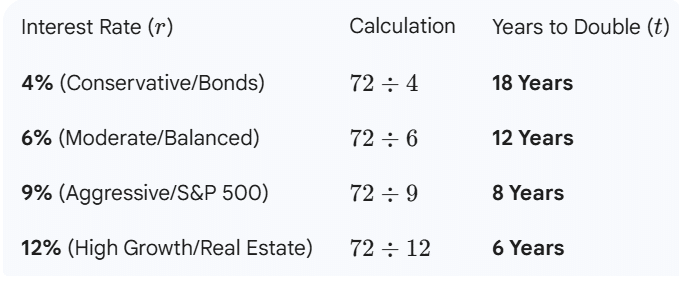

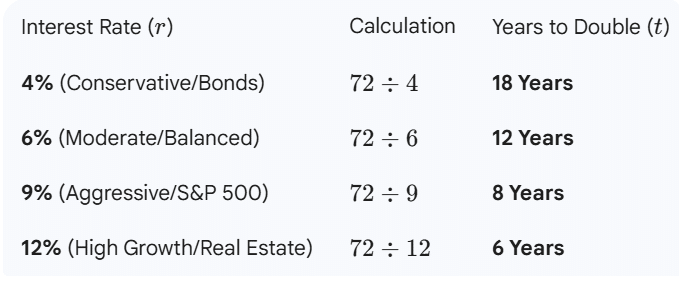

The Rule of 72 – Wealth Building Secret

This calculation provides an easy way to find out how long it will take to double an investment, if you know the anticipated rate of return or interest rate.

Divide the expected rate of return by 72, and this gives you an estimate of how long it will take your money to double. For example, with an expected annual rate of return of 10%, it will take roughly 7.2 years for your investment to double.

Time (in years) until investment is doubled = 72/annual rate of return

If you invest $500,000 in an investment which earns 10% annually, you’ll double your money in approximately seven years.

The rule of 72 illustrates the power of compound interest.

How Long it Takes to Double Your Money

1. The Core Variables

Before picking an investment, consider these three things:

- Risk Tolerance: This is the “sleep at night” factor. High-risk paths (like individual stocks or crypto) can double money quickly but can also lead to steep losses. Low-risk paths (like bonds) deliver more stable returns, but slow growth.

- Time Horizon: The “Rule of 72” is the best tool here. Divide 72 by the expected annual return to see how many years it takes to double:

- At 7% return (Historical stock market average after inflation): ~10.3 years.

- At 10% return (S&P 500 historical average): ~7.2 years.

- At 4% return (Conservative bonds/HYSA): 18 years.

- Investment Savvy: Do you want to be a “passive” passenger or an “active” pilot? Passive investors should stick to Index Funds; active investors might look at real estate, active investing strategies or business ventures.

Your financial goals, risk tolerance and willingness to spend time educating yourself in investing strategies will drive your decision. After decades of investing, studying the investment research and the markets, the data is clear. Most active investors typically underperform the market indexes. Check out our historical asset class performance article to understand how the market indexes have performed over time.

2. Strategies to Double $500k

Here are four distinct paths, ranging from conservative to aggressive.

Path A: The “Conservative Path” (Bonds and Cash predominantly)

- The Strategy: Invest the $500k into a conservative asset allocation of roughly 75% bonds/high yield cash and 25% broad-market ETF (like VTI or VOO) that tracks the total US stock market or S&P 500 or VT, Vanguard Total World Stock Index Fund ETF, which provides access to the entire world stock market within one fund.

- Potential Gains: Historically 4-5% annually.

- Risks: Declining interest rates can hurt long term capital appreciation.

- Timeline to $1M: 14-18 years.

Path B: The “Balanced Shield” (60/40 Portfolio)

- The Strategy: 60% Stocks, 40% Bonds. This is for the reader with a lower risk tolerance and less interest in stock picking and portfolio management.

- Potential Gains: Generally, 5–7% annually, depending upon the performance of the financial markets.

- Risks: Lower growth. Inflation risk could stifle growth when your money grows, but its purchasing power doesn’t keep up with the cost of living. Stock market declines can also hinder how long it’ll take to double your money.

- Timeline to $1M: 10-14 years.

This is the path that my family has taken over years, with adjustments in the asset allocation from 60% stocks / 40% bonds to more aggressive 70%/30% allocations. Over decades, with regular additions into our financial accounts, compounding has worked its magic.

Path C: The “Lumberjack” (Real Estate Leverage)

- The Strategy: Instead of buying one property with cash, use the $500k as 25% down payments on four $500k rental properties (totaling $2M in real estate).

- Potential Gains: You aren’t just gaining on your $500k; you are gaining appreciation on the full $2M value. A 5% increase in property value ($100k) is a 20% return on your actual cash. The leverage of borrowing to help pay for the properties can rapidly increase returns, in a strong market.

- Risks: Leverage is a double-edged sword. If property values drop, you still owe the full mortgage. There is also “tenant risk” and maintenance costs.

- Timeline to $1M: Could be 5 years or less, depending on appreciation and mortgage pay-down.

Other issues to consider with this real estate strategy are finding properties that are fairly priced and affordable. On the east and west coasts, real estate costs are sky-high and it’s tough to find a rental property for $500,000. Higher mortgage rates will lower your returns as well. This type of strategy is better in areas with more affordable real estate, with a strong rental market. If you can provide “sweat equity” for repairs and maintenance and have the time to manage the properties yourself, you’ll boost your financial potential.

Also, real estate investments are less liquid than investing in the financial markets, where you can buy and sell stock and bond funds with the click of a button.

Path D: The “Speculator” (Alternative Assets)

- The Strategy: Allocating a portion (e.g., 10–20%) into high-growth, high-volatility assets like Bitcoin, early-stage startups (Angel investing), alternative investments or sector-specific tech stocks and riskier growth stocks and funds.

- Potential Gains: 20%+ or even “10x” returns.

- Risks: Extreme. You could lose the entire principal of that portion. This should only be done with a percent of your net worth, as you could risk great losses.

- Timeline to $1M: Could be 1–3 years (or never).

Typically, I suggest that more aggressive investors deploy 5 to 10% of their investable assets into riskier investments. This provides the opportunity for high returns and capped losses. Some alternative investments are illiquid, so you’ll need to keep your capital invested for long periods of time, before realizing potential gains.

Pro Tip: Keep some cash on the side, so when stocks, crypto, alternatives and other investments take a dive, you can pick up shares at bargain prices. This enables greater future growth potential.

3. Comparison Table

| Strategy | Risk Level | Expected Return | Est. Time to Double |

| High-Yield Savings/CDs/short term bond funds | Very Low | 4–5% | 14–18 Years |

| Stock and bond ETF portfolios | Moderate | 8–10% | 7–9 Years |

| U.S. and international stock and bond ETF portfolios | Moderate-high | 9-11% | 6.5-8 Years |

| Real Estate (Leveraged) | High | 11–14% (Inc. Equity) | 5–7 Years |

| Aggressive Growth/Crypto | Very High | Variable | 1–5 Years |

Realize that no returns are guaranteed. We use prior returns to predict the future, but the future returns are unknowable. The riskier the investment, the greater chance of outsized gains and losses.

4. Immediate Steps to Take

- Max Out Tax-Advantaged Accounts: If you are still working, and have access to a 401k, 403b or IRA, make sure to contribute as much as you can. If your employer matches your 401k or 403b investment, contribute at least the necessary amount to receive the employer match.

- Assess “The Gap”: If you want to double your money in 5 years but only have a “Conservative” risk tolerance, your goals and reality are mismatched. You must either increase your risk tolerance or extend your timeline.

- Minimize Fees: A 1% management fee might seem small, but on $500k, that’s $5,000 a year gone. Over 10 years, that eats a massive chunk of the compounding effect.

Investing Resources to Help Increase Your Net Worth

Recommended Tools for Today’s Economy

- Empower: Free tracker for net worth, investment allocation, and retirement projections. (I use the free tools)

- Groundfloor: Real estate investing with small minimums—even in IRAs (I have an account)

- M1 Finance: Automate investing and easily rebalance with no management fees (I have an account)

- Vaulted: Invest in real gold and silver with low fees and minimums.

- Free Microbook: “Invest and Grow Your Wealth”: Actionable advice for smarter investing

Related

- How To Invest $500,000 For Income and Growth?

- Can I Retire At 60 With $500,000?

- Robo-Advisor VS Target Date Fund – Which Investment Strategy Is Right For You?

- The Magic of Compounding Stocks-Get Rich While You Sleep

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

The post How To Double Your Net Worth Of $500,000 To $1 Million appeared first on Barbara Friedberg.